BTC Down 40%: What Happens to My Loan?

This is the first question serious holders ask before borrowing against Bitcoin. Not “what’s the interest rate,” but what happens if the market moves sharply against me.

A 30-40% drawdown in BTC is not a tail risk. It is a normal market event. Any borrowing strategy that cannot tolerate that move is structurally flawed.

This article explains what actually happens when Bitcoin drops after you borrow against it, how liquidation mechanics work in DeFi, and how conservative borrowing absorbs volatility rather than amplifying it.

Key Takeaways

- Bitcoin volatility does not automatically lead to liquidation. Liquidation occurs when LTV thresholds are breached, not when price drops.

- At a 20% LTV, Bitcoin can fall 40% and your position remains well within safe range.

- Conservative borrowing absorbs volatility, preserves exposure, and maintains optionality. For more active users, risk must be actively managed, but the rules are transparent and predictable.

- Self-repaying loan structures reduce risk over time by shrinking the loan balance automatically, widening your safety buffer even in flat or declining markets.

- Borrowing against Bitcoin is not about avoiding risk. It is about choosing which risks you accept and structuring around them.

Start With the Right Frame: Borrowing Is About Ratios, Not Price

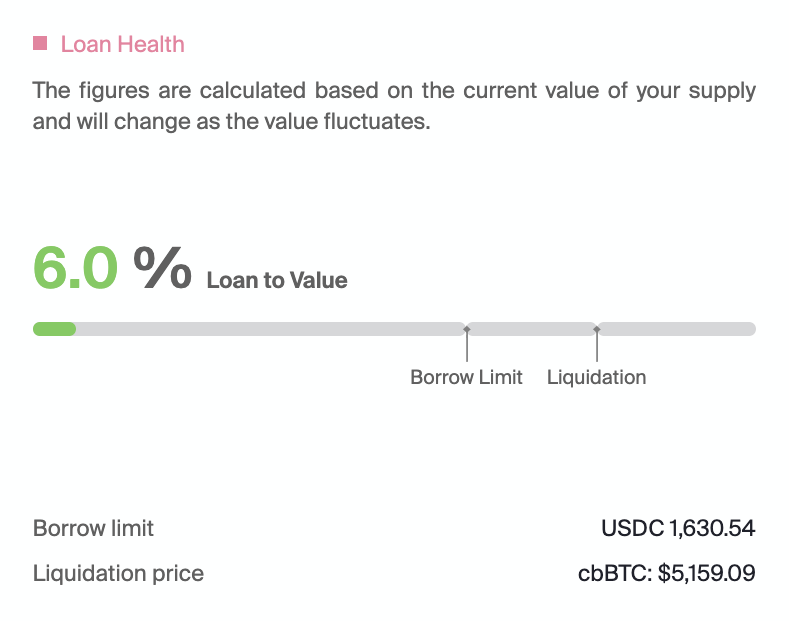

When you borrow against Bitcoin, the key variable is not the price of BTC. It is the loan-to-value ratio (LTV).

LTV measures how much you borrow relative to the value of your collateral. If you deposit $100,000 worth of BTC and borrow $20,000, your LTV is 20%.

Price moves affect your LTV, not your loan directly. A drop in BTC increases LTV. Liquidation only occurs if LTV crosses a predefined threshold.

This distinction is critical. Most liquidation fears come from thinking in price terms instead of ratio terms.

What Actually Happens in a 30-40% BTC Drawdown

Let’s walk through a simplified example.

You deposit $100,000 of BTC. You borrow $20,000 in USDC. Your initial LTV is 20%.

Now Bitcoin drops 40%.

Your collateral value falls to $60,000. The loan remains $20,000. Your new LTV is 33%.

At this point, nothing happens.No forced action. No liquidation.

Most DeFi lending protocols have liquidation thresholds well above this level. The system is designed to absorb volatility as long as borrowing is conservative.

A 30-40% drawdown feels dramatic in price terms, but at low LTVs it is structurally manageable.

When Liquidation Risk Actually Appears

Liquidation risk increases as LTV approaches the protocol’s liquidation threshold.

- Borrowing at 15-25% LTV leaves a wide safety buffer.

- Borrowing at 50-60% LTV leaves little room for volatility.

Liquidation is not binary and it does not mean losing everything. In DeFi, liquidations are typically partial, designed to restore the position to a safe LTV rather than wipe out the collateral.

This is why initial loan sizing matters far more than short-term price moves.

Why Conservative Borrowing Changes the Outcome

The most important risk decision happens at loan origination.

Borrowing conservatively is not about timing the market. It is about designing a position that can survive normal volatility without intervention.

For long-term Bitcoin holders, a conservative LTV:

- Absorbs drawdowns without forcing action.

- Reduces the likelihood of liquidation during fast moves.

- Aligns borrowing with multi-year holding horizons.

Borrowing aggressively may look efficient in calm markets, but it converts normal volatility into existential risk.

The Role of Yield and Self-Repaying Structures

Traditional borrowing leaves the loan balance static unless the borrower actively repays it.

More advanced structures reduce risk over time by allowing collateral to generate yield that pays down the loan balance. As the loan decreases, LTV improves, creating a widening safety buffer even if prices stagnate.

This matters most during prolonged holding periods, where time becomes an ally rather than a liability.

The key point is not yield chasing, but risk decay. A loan that shrinks over time becomes structurally safer.

What Borrowers Can Do During a Drawdown

If Bitcoin drops sharply, borrowers generally have three options, depending on their position:

Do nothing. At conservative LTVs, this is often the correct response.

Add collateral. Topping up collateral lowers LTV and restores your buffer.

Partially repay the loan. Reducing the loan amount has the same effect.

The ability to choose is itself the advantage. Selling removes optionality. Borrowing preserves it.

What This Means for Long-Term Holders

A 30-40% Bitcoin drawdown is not a failure case. It is a design constraint.

Borrowing against BTC only becomes dangerous when it is structured as a short-term, high-leverage trade. For long-term holders using conservative LTVs, volatility is expected and accounted for upfront.

The question is not whether Bitcoin can drop. It is whether the borrowing structure was built to tolerate it.

Built for Volatility, Not Against It

Altitude aggregates rates across established protocols like Aave and Morpho, while activating idle collateral to generate yield that automatically reduces your loan balance over time. Conservative LTVs, transparent on-chain mechanics, and self-repaying structures mean your position is designed to weather drawdowns, not just survive them.