For long-term Bitcoin and Ethereum holders, needing liquidity often creates a practical problem. Selling provides cash, but it also triggers taxes, ends market exposure, and unwinds a position built over years. Common situations, such as a property purchase, business expense, or tax obligation, force holders to evaluate whether selling is actually the right default.

For many holders, it is not. Increasingly, they are turning to crypto-backed loans as a way to access liquidity without exiting positions they intend to hold long term.

This article examines the trade-offs between selling and borrowing, explains how DeFi borrowing works in practice, and outlines why borrowing platforms like Altitude are designed as professional tools for accessing liquidity without sacrificing long-term conviction.

The Real Cost of Selling Crypto

Selling crypto is operationally simple, but its full cost is often underestimated.

In most jurisdictions, selling Bitcoin or Ethereum triggers capital gains tax. For holders with a low cost basis, this can mean giving up a meaningful portion of gains immediately. Once sold, that capital is permanently removed from the position, and re-entering later often comes at higher prices and a reset cost basis.

There is also the cost of lost upside. Selling ends participation in future appreciation. Many long-term holders experienced this during previous market cycles, where assets recovered after periods of uncertainty, leaving sellers on the sidelines.

Finally, selling breaks the original investment thesis. Long-term positions are typically built with multi-year conviction. Unwinding them for short-term liquidity introduces friction that often proves difficult to reverse.

Selling can still be the right decision in some cases, but it should be treated as a deliberate choice rather than the default.

Borrowing Against Crypto as an Alternative

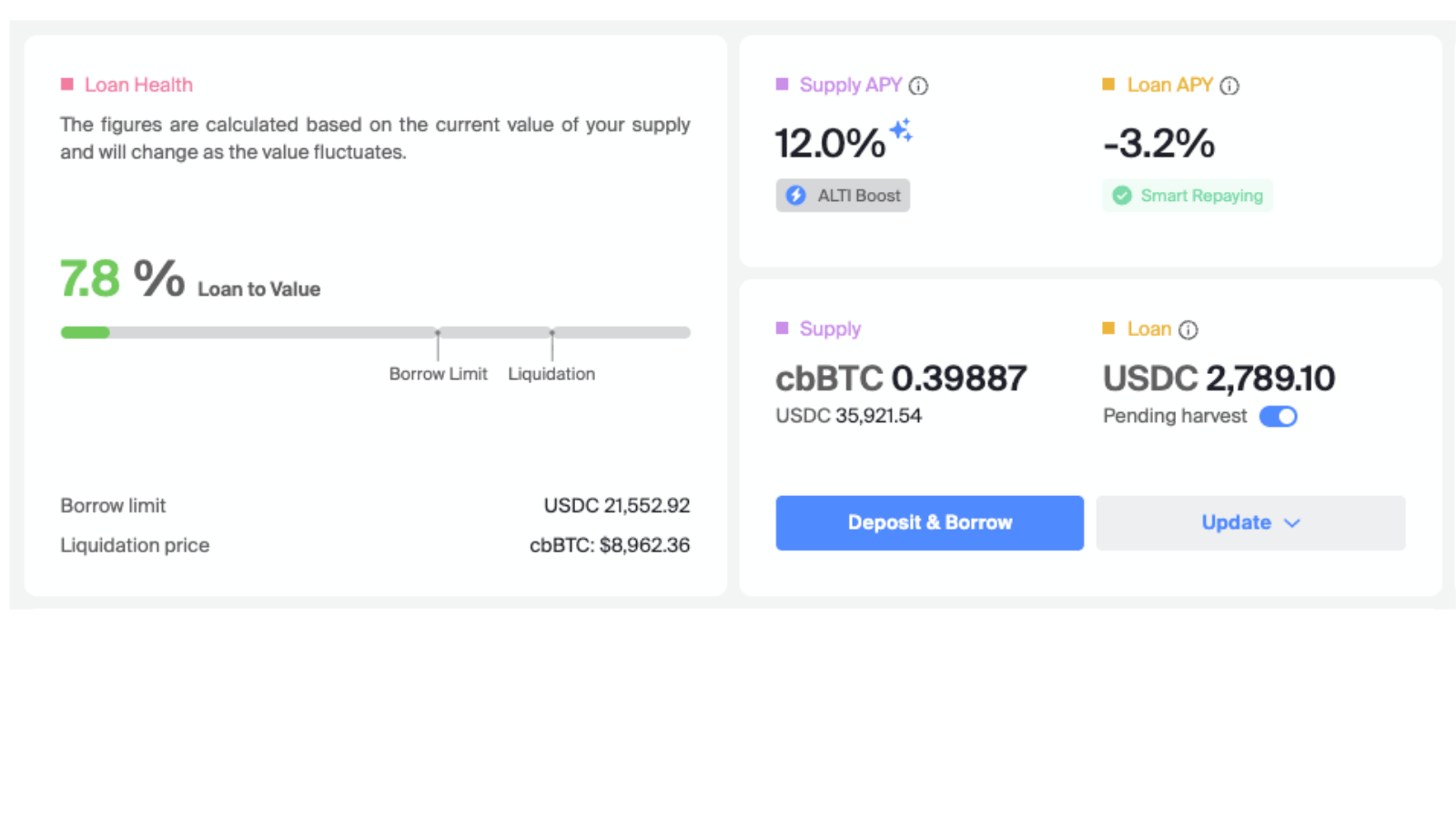

Borrowing against crypto allows holders to deposit BTC or ETH as collateral and borrow stablecoins such as USDC against it. Instead of selling the asset, liquidity is unlocked while ownership and market exposure are preserved.

In DeFi, this process is non-custodial and governed by smart contracts. Protocols like Aave and Morpho define collateral requirements, interest rates, and liquidation thresholds transparently and enforce them automatically on-chain.

Because borrowing does not involve selling the underlying asset, it typically does not trigger a taxable event at loan creation. When the loan is repaid, the collateral can be withdrawn, ideally after having appreciated during the loan period.

This structure makes DeFi borrowing particularly relevant for long-term holders who view BTC and ETH as capital rather than trading instruments. Learn more about how crypto-backed loans work.

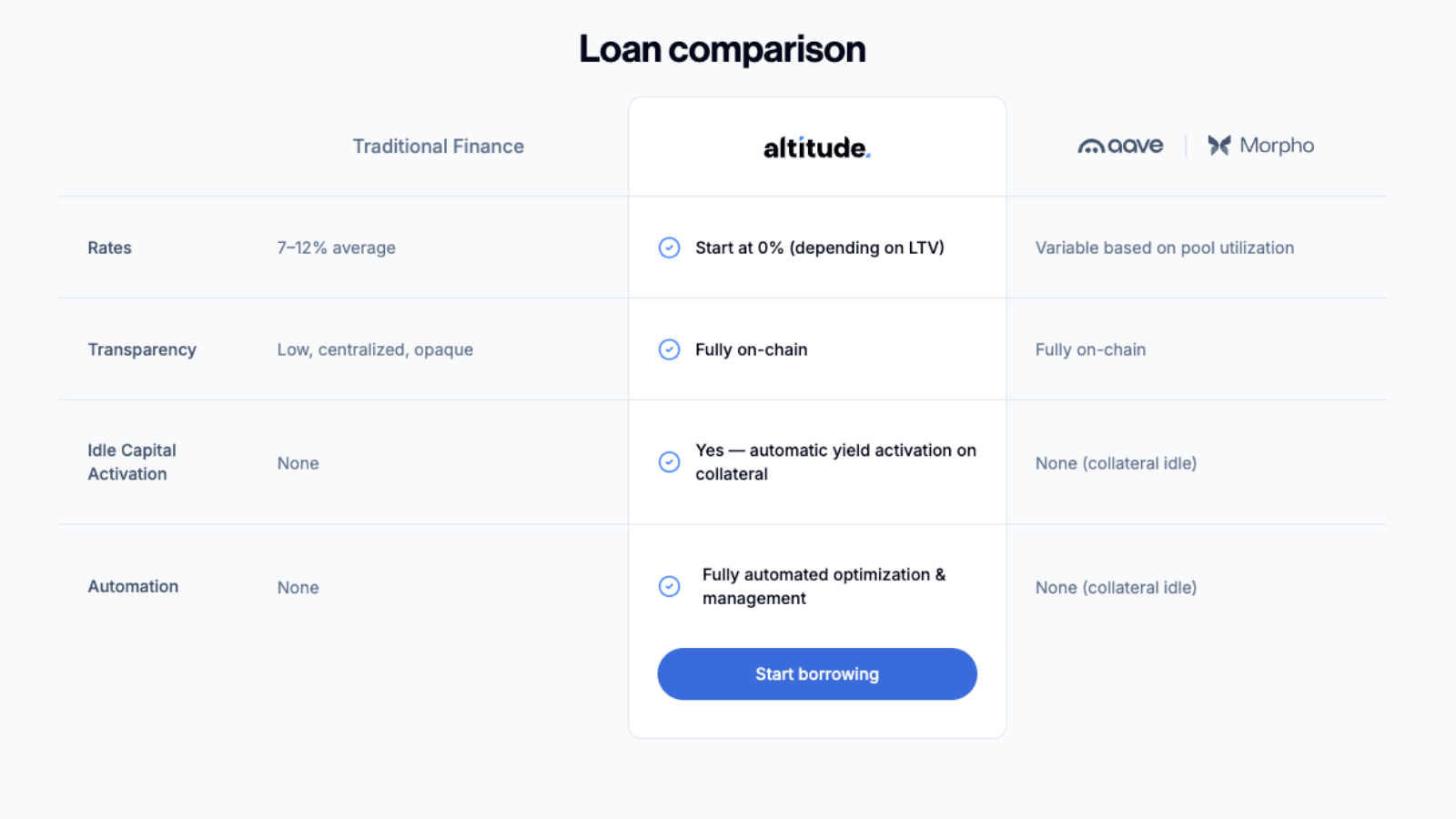

DeFi Borrowing vs Centralized Crypto Loans

Not all crypto-backed loans are equivalent.

Centralized lenders require users to transfer custody of their assets. The failures of several major lenders in 2022 highlighted the risks of this model. When custody is surrendered, users are exposed to counterparty risk that may only become visible during periods of stress.

DeFi lending protocols operate differently. Assets remain on-chain, governed by transparent rules enforced by code rather than by institutions. Liquidations, interest rates, and collateral ratios are visible and predictable.

For long-term holders who prioritize control and transparency, this distinction is fundamental.

The Limitation of Traditional DeFi Borrowing

While DeFi borrowing solves many of the issues associated with selling, it has historically introduced a different inefficiency.

In most lending protocols, collateral remains idle while securing the loan. Borrowers pay interest, but their deposited assets do not actively reduce the cost of borrowing.

For holders planning to maintain positions over long time horizons, this creates unnecessary drag. Capital is preserved, but not fully utilized. This is the problem Altitude was built to address.

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Consult a qualified professional regarding your specific situation.